Nigeria ranks nine among countries that owns digital currency

. UNCTAD issues measures to curb crypto currency in developing nations

By Fredrick Wright

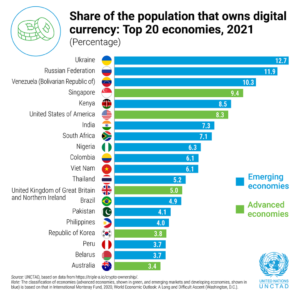

Nigeria has been ranked the ninth position among nations that holds higher percentage of population that owns digital currency.

The United Nations Conference on Trade and Development (UNCTAD), in its latest report obtained by SlyeNews said 6.3 percent of Nigeria’s population own digital currency.

Ukraine tops the chart with 12.7 per cent of its population while Russia, Venezuela and Singapore followed with 11.9m 10.3 and 9.4 per cent of the population accordingly.

Kenya tops the African char with 8.5 per cent, while South Africa followed with 7.1 and Nigeria 6.3 per cent.

While these private digital currencies have rewarded some, and facilitate remittances, they are an unstable financial asset that can also bring social risks and costs.

UNCTAD has released three policy briefs that delve into these risks and costs, including the threats crypto currencies bring to financial stability, domestic resource mobilization and the security of monetary systems.

The policy brief entitled “All that glitters is not gold: The high cost of leaving crypto currencies unregulated” examines the reasons for the rapid uptake of crypto currencies in developing countries, including facilitation of remittances and as a hedge against currency and inflation risks.

Recent digital currency shocks in the market suggest that there are private risks to holding crypto, but if the central bank steps in to protect financial stability, then the problem becomes a public one.

If crypto currencies become a widespread means of payment and even replace domestic currencies unofficially (a process called cryptoization), this could jeopardize the monetary sovereignty of countries.

UNCTAD has therefore urged authorities to take the following actions to curb the expansion of crypto currencies in developing countries:

“Ensure comprehensive financial regulation of crypto currencies through regulating crypto exchanges, digital wallets and decentralized finance, and banning regulated financial institutions from holding crypto currencies (including stablecoins) or offering related products to clients.

“Restrict advertisements related to crypto currencies, as for other high-risk financial assets.

“Provide a safe, reliable and affordable public payment system adapted to the digital era.

“Agree and implement global tax coordination regarding crypto currency tax treatments, regulation and information sharing.

“Redesign capital controls to take account of the decentralized, borderless and pseudonymous features of crypto currencies,” it stated.